In today's inaugural edition, we're diving deep into the latest macroeconomic data to help you navigate the complex global economic landscape. Our mission is to provide you with clear, actionable insights by analyzing key economic indicators and their implications for markets and investment decisions.

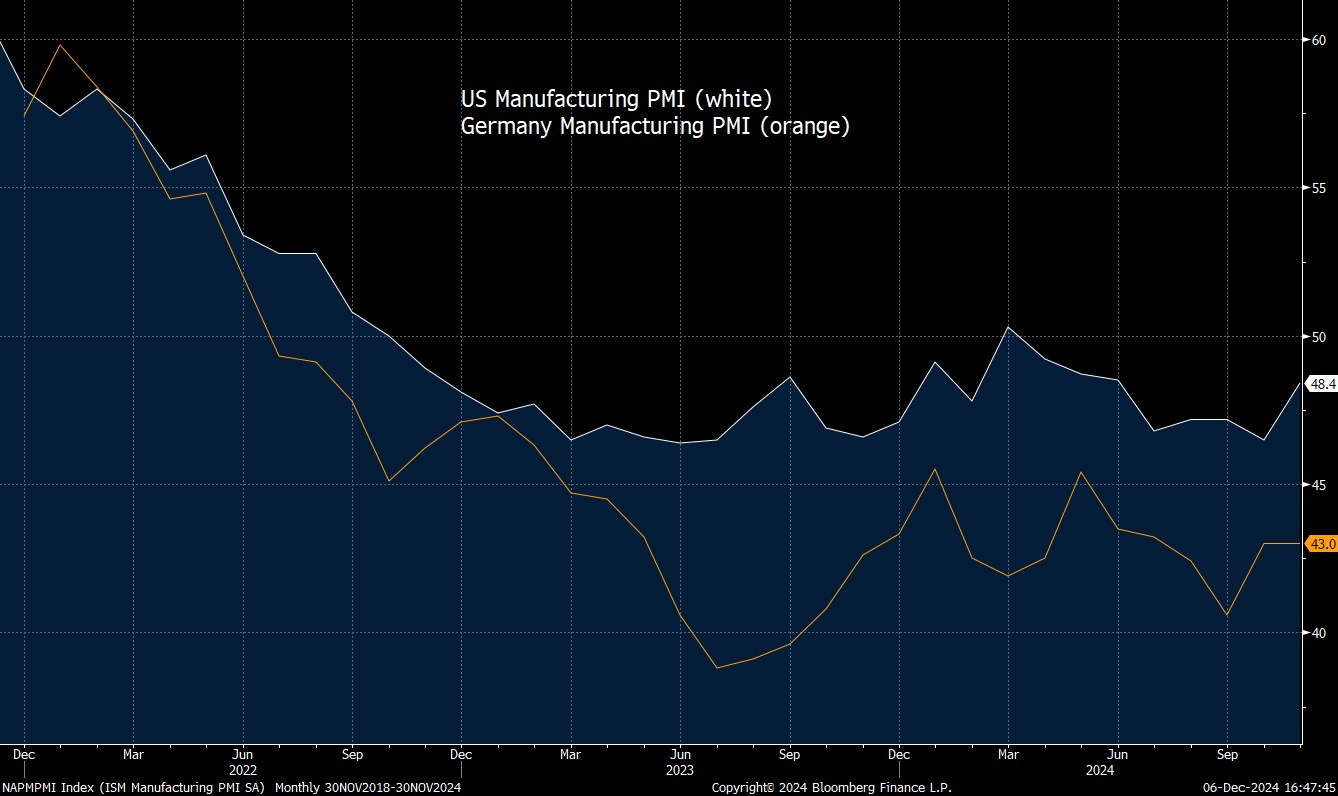

Let's start with one of the most watched economic indicators - the Manufacturing PMI data, which gives us crucial insights into the industrial sector's health across major economies.

The US Manufacturing PMI reached its lowest point before Germany's Manufacturing PMI did, highlighting a divergence in industrial sector performance between these major economies. Both indices currently remain below the critical 50-point threshold, which separates expansion from contraction.

Germany's manufacturing sector appears to be facing particularly significant challenges in its recovery trajectory, with persistent weakness in industrial activity. The timing of these downturns is noteworthy: while the US Manufacturing PMI only dipped below 50 in November 2022, Germany had already entered contractionary territory several months earlier, in July 2022. This earlier onset and prolonged duration of manufacturing weakness in Germany suggests deeper structural challenges in its industrial sector compared to the United States which appears to be on a recovery track.

While Manufacturing PMI remains below 50, U.S. Services PMI holds at 52.1. In contrast, Services readings across all major EU economies are below 50 in both sectors, suggesting potential shorting opportunities in the European stock markets.

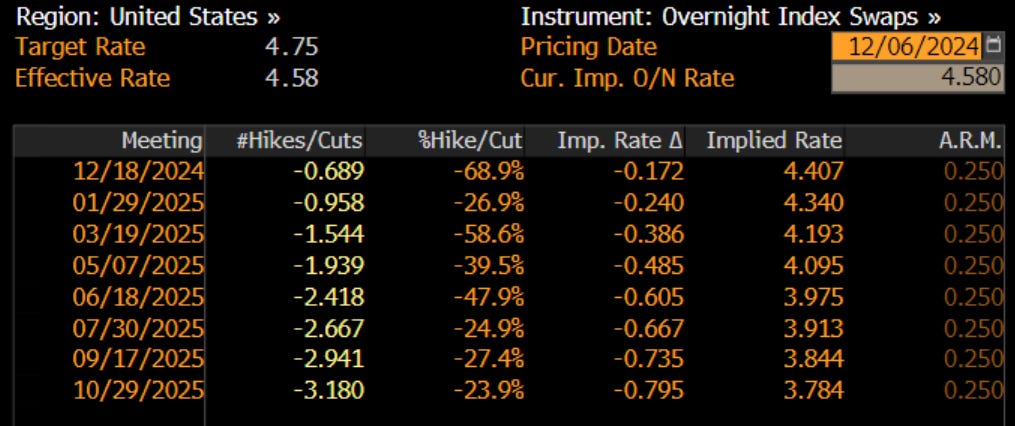

According to the recent FED minutes, Federal Reserve Won’t Cut Every Meeting: Unless the economy heads toward a recession, the Fed may only lower interest rates modestly as it calibrates them toward its estimate of the neutral rate, with the labor market holding the keys to the Fed’s reaction function. The FED is anticipated to cut rates one more time on the 18th of December 2024 with a probability rate of 68.9%.

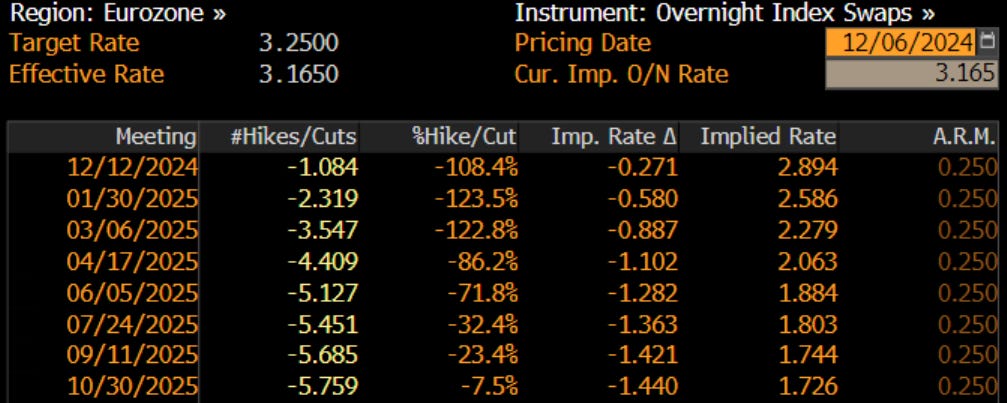

Based on current ECB rate probabilities, market expectations strongly indicate that the European Central Bank will implement consecutive rate cuts at every monetary policy meeting through June 2025. This aggressive rate-cutting path reflects growing concerns about economic growth in the Eurozone and the need to support economic recovery.

However, this anticipated approach raises important considerations. While the ECB maintains its commitment to data-dependent decision-making, current economic indicators suggest a more cautious approach might be warranted. Specifically, with inflation showing signs of persistence and moving sideways rather than decisively downward, an aggressive rate-cutting cycle could potentially undermine price stability objectives.

OPEC+ has made significant strategic adjustments to its production plans, with several key developments shaping the oil market outlook. The organization has implemented a three-month delay in its output revival, pushing the first production increase to April. This decision is part of a broader strategy that extends the unwinding of production curbs until September 2026, representing a more gradual approach than initially planned.

The decision comes amid challenging market conditions, particularly influenced by two major factors: weak demand growth in China and increasing oil supply from the United States. This marks the third consecutive delay in output hikes, reflecting ongoing market uncertainties. Adding to this, the United Arab Emirates has separately announced a modification to its production plans, extending its planned increase over 18 months instead of the original nine-month timeline.

Market reaction to these decisions has been relatively muted, as participants had largely anticipated some form of delay in production increases. This is evidenced by oil futures maintaining stable trading patterns within a confined range.

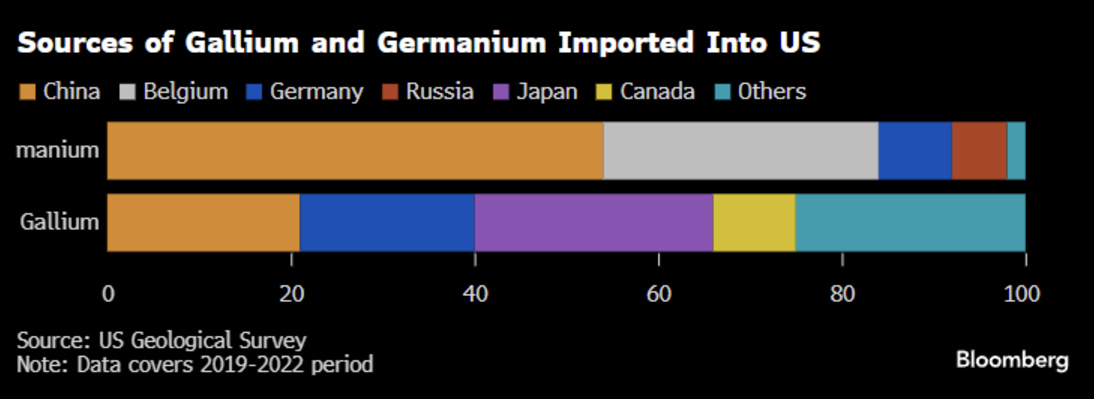

China banned exports of key high-tech materials to the US in response to Biden's technology restrictions.

The ban covers gallium, germanium, antimony, and superhard materials, with tighter controls on graphite. This came after US restrictions on high-bandwidth memory chip sales to China.

The impact is significant - a Chinese ban on gallium and germanium alone could cost the US economy $3.4 billion. These metals are crucial for semiconductors, satellites, and military equipment.

"Export bans are intended as a warning," noted Joe Mazur from Trivium China, indicating China's stronger stance against US economic pressure.

The effects are already visible - China's exports of gallium and germanium to the US dropped to zero this year, while antimony exports remain minimal.

Chinese industry groups have advised local companies to be cautious when purchasing US chips.

Facing heightened security challenges, the EU is planning a dramatic increase in defense spending, aiming to nearly double annual budgets to $720 billion. This surge reflects a commitment to address decades of underinvestment that left European NATO members reliant on U.S. support and vulnerable to modern threats. Ground forces are particularly depleted, driving an estimated $200 billion investment in tanks, artillery, and infantry fighting vehicles, alongside fighter jets and air defense systems.

While European manufacturers like Airbus and Rheinmetall will benefit, the region’s limited production capacity and urgent needs mean U.S. defense contractors are poised to play a critical role. Lockheed Martin’s F-35 fighter jets, already selected by Romania and other NATO members, dominate Europe’s modernization efforts, with contracts exceeding $7 billion. Boeing stands to gain from increased demand for its Apache helicopters, such as Poland’s $12 billion order for 96 units, and its P-8 Poseidon maritime patrol aircraft, valued at $175 million each. RTX's Patriot missile systems, which Poland alone has invested $29.5 billion in, are also integral to bolstering air defenses.

The ripple effects of this investment surge will significantly boost U.S. Aerospace & Defense companies. We are currently analyzing these companies to determine which ones should be included in our investment portfolio.

Looking ahead, next week brings economic data releases that will shape market sentiment. We'll be closely monitoring three key indicators:

Our current market outlook remains cautiously optimistic. While historical data suggests December typically performs well after two consecutive years of positive Dow returns, we advocate for a balanced approach.

"We maintain a bullish stance while keeping a diversified portfolio of both long and short positions to manage potential volatility."